Germany

Total employment in the OECD returned to pre-crisis levels at the end of 2021 and continued to grow in the first months of 2022. The OECD unemployment rate gradually fell from its peak of 8.8% in April 2020 to a level of 4.9% in July 2022, slightly below the 5.3% value recorded in December 2019. However, the labour market recovery has been uneven across countries and sectors and is still incomplete, while its sustainability is challenged by the economic fallout of Russia’s unprovoked, unjustified, and illegal war of aggression against Ukraine.

Germany’s job market is strong compared with other OECD countries. The unemployment rate stood at 2.9% in July 2022, which is below the OECD average of 4.9%, and also below Germany’s rate of 3.1% in December 2019.

Germany’s employment challenge is that workers work short hours: average hours worked per worker in Germany are lower than in any other of the 38 OECD countries. Workers work 21% fewer hours in Germany than on average in the OECD. Some of these short work hours are involuntary or policy-induced.

Increasing the number of hours worked of workers who are in part-time or non-standard employment in Germany would reduce labour shortages and be both growth-enhancing and inflation-dampening. Policy can in particular promote the hours worked by women, and of low-skilled and older workers. Additional avenues are to boost skilled labour migration and to make it easier for refugees from Ukraine to work, for example through better provision of childcare facilities.

Vacancies surged to record highs in the OECD area, and reports of labour shortages rose significantly in many industries and countries. Despite this, nominal wage growth remains well below the high inflation induced by the commodity price hikes spurred by Russia’s war of aggression against Ukraine. Real wages in OECD countries are expected to continue to decline over the course of 2022, as inflation is projected to remain well above the negotiated nominal wages for 2022.

Vacancies and labour shortages are high in Germany. Germany’s Federal Employment Agency reported 862 700 job vacancies for August 2022, up by 22% from December 2019. July and August 2022 are, however, also the first two months since the plunge in 2020 due to COVID-19 that the number of job vacancies has declined in two consecutive months. Compared with the four years before the COVID-19 pandemic, the share of Germany’s manufacturing firms reporting production constraints due to labour shortages doubled from 19% to 38% in the second quarter of 2022, and for services firms this share rose from 25% to 40%.

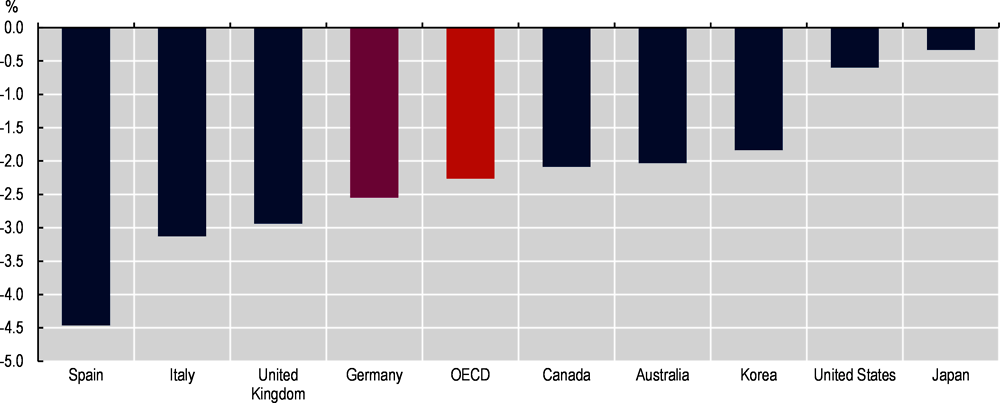

Average real wages for German workers are expected to shrink by 2.6% in 2022 (Figure 1), with inflation climbing to 7.2% in 2022. The predicted fall in real wages is slightly larger than for the OECD as a whole. A better picture emerges for low-wage earners: the real value of Germany’s minimum wage increased by 1.2% over the 12 months to July 2022.

Collective wage negotiations and the “Concerted Action” group – which involves the government, trade unions and employer associations – have an important role to play to ensure that no wage-price spiral will be set in motion in Germany and that vulnerable groups can cope with the higher costs of living. One approach – practised by Germany’s chemical sector, and also in related ways in Italy and the Netherlands – is to provide a one-time payment for all employees, which in percentage terms is a larger bonus for the lower-paid.

Source: OECD Economic Outlook 111 database; and OECD calculations.

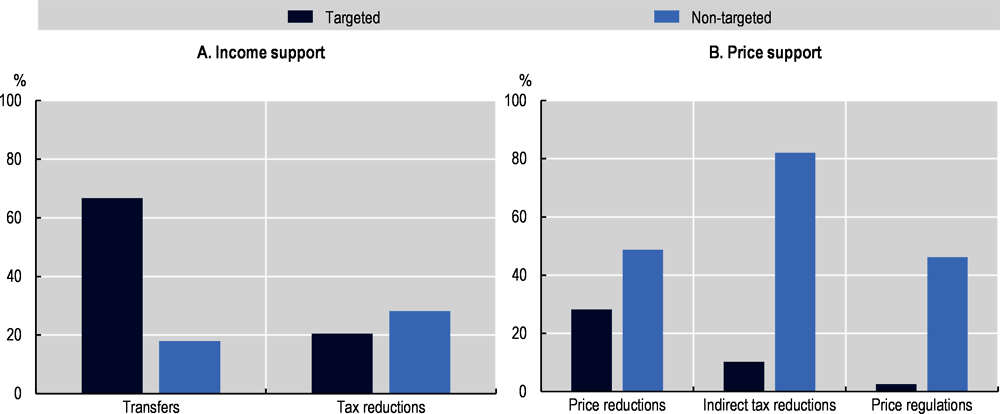

Russia’s war against Ukraine has brought new challenges. It has contributed to the highest inflation in decades, notably through price increases for energy and commodities. Low-income households, who spend a large share of their tight budgets on energy and food, are particularly affected. On average, for the OECD countries for which data are available, households in the bottom income quintile spend 50% more of their consumption budget on food and energy than those in the top income quintile. Targeted support, which often takes the form of transfers (Figure 2), involves lower fiscal costs, expands demand less at a time of high inflation and is better in line with the green transition.

Energy prices in Germany have surged. Dependence on energy imports from Russia is high: before the beginning of Russia’s war against Ukraine, one-third of Germany’s energy supply came from Russia. Germany’s economy is thus facing the challenge to reorient energy sources and the risk of acute supply disruptions, which would test the resilience of the labour market.

Germany’s supplementary budget for 2022 contained additional spending of 1.1% of GDP to mitigate the energy price surge. It included a fuel tax cut for three months, an increase of the commuting subsidy, public transport subsidies, the permanent abolishment of the renewable energy surcharge, as well as several one-off cash transfers and income tax reliefs for households. On 4 September 2022, the government announced a new energy support package estimated at 1.8% of GDP. Measures to support household incomes include one-off cash transfers to students and pensioners, increases in housing allowances, child benefits and basic social transfers, a reduction in the social security contributions of low earners and inflation-adjusted shifts to the nominal income tax thresholds.

The new relief measures are better targeted at vulnerable households, which need support the most: in Germany, the bottom 20% in the income distribution spend 23% of their expenditures on energy and food, compared to 15% for the top 20%. Some of the past measures, including the fuel tax cut, disbursed considerable amounts of public resources to all households. Such a fiscal boost reduces incentives to save energy and stands in contrast to Germany’s other initiatives that aim to reduce energy consumption for climate change and energy security reasons.

Note: Based on data for 35 OECD countries plus Bulgaria, China, India and Romania. Targeted measures are means-tested or benefit certain categories of consumers based on their energy consumption or other criteria. Non-targeted measures apply to all consumers with no eligibility conditions.

Source: OECD (2022), OECD Economic Outlook, Volume 2022 Issue 1, https://doi.org/10.1787/62d0ca31-en; and OECD calculations.