United States

Total employment in the OECD returned to pre-crisis levels at the end of 2021 and continued to grow in the first months of 2022. The OECD unemployment rate gradually fell from its peak of 8.8% in April 2020 to a level of 4.9% in July 2022, slightly below the 5.3% value recorded in December 2019. However, the labour market recovery has been uneven across countries and sectors and is still incomplete, while its sustainability is challenged by the economic fallout of Russia’s unprovoked, unjustified, and illegal war of aggression against Ukraine.

After reaching one of the highest pandemic-period peaks across OECD countries (14.7% in April 2020), the unemployment rate in the United States returned to its pre-crisis level of 3.6% in March 2022, where it has remained (Figure 1), edging up slightly to 3.7% in August 2022.

The high peak unemployment rate highlights the differences in the policy path the United States took to manage the COVID-19 crisis. While many other OECD countries relied on job retention schemes, which reduced hours but kept workers connected to jobs, the United States relied on (often temporary) lay-offs to reduce working time, as well as enhanced unemployment benefits.

The labour market rebound has been particularly robust in the United States, spurred by the need to re-fill positions temporarily closed after the various waves of the pandemic together with the strong growth in product demand observed since the second half of 2021.

Looking forward, there is concern over a potential labour market mismatch. The quits rate in the United States reached record highs in the second half of 2021 and remained high in the first months of 2022. Job vacancies have also remained high. Evidence suggests that the current employment shortfall is due to increased inactivity among older workers, a deep and persistent fall in employment among mothers of young children, and shifting worker preferences amid strong labour demand. In particular, workers in low-skill jobs may be more sensitive to poor working conditions and low pay.

Note: Latest month available refers to May 2022 for the United Kingdom and to August 2022 for the United States.

Source: OECD (2022), “Unemployment rate” (indicator), https://doi.org/10.1787/52570002-en (accessed on 2 September 2022).

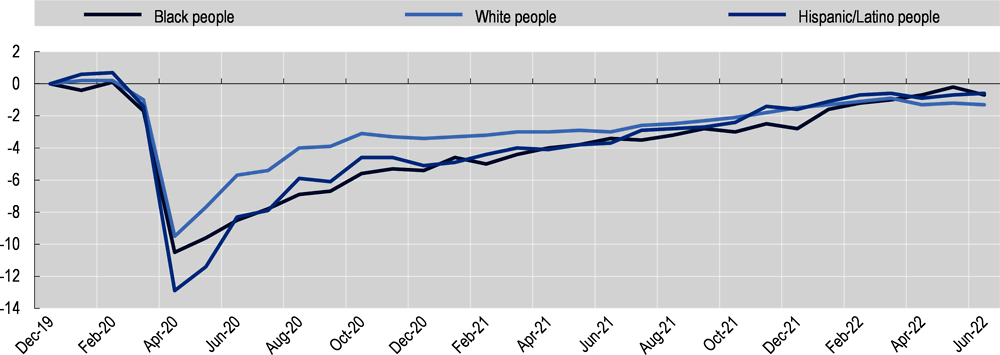

Few OECD countries collect data, which allow the impact of the crisis on racial/ethnic minorities to be monitored. In most of those which do, the crisis affected racial/ethnic minorities disproportionally and, where information is available, the recovery of these groups has been slower. However, there are countries that fare better in this respect, showing that a worse impact for minorities is not a fatality: in New Zealand, racial/ethnic minorities have benefited from the recovery more than the majority group, reducing their employment gap in Q4 2021 relative to Q4 2019.

In the United States, the main racial/ethnic minorities were more affected by the initial impact of the crisis, and lagged behind in the recovery until December 2021. At the onset of the crisis in April 2020, the (seasonally adjusted) employment-to-population ratio fell by 13 percentage points for Hispanic/Latino people and 10.5 percentage points for Black people (Figure 2), compared to 9.55 percentage points for white people.

The higher likelihood of employment loss for racial/ethnic minorities was only partially explained by their sectoral and occupational concentration, i.e. minority workers were more likely to lose their employment than white workers in the same industries and occupations over the course 2020. Indeed, more generally, observable characteristics explain little of the highly persistent labour market disparities between Black people and white people in the United States.

Both Black and Hispanic/Latino people lagged behind white people for most of the recovery (Figure 2). In particular, relative to white people, employment losses for Hispanic/Latino people remained larger until Q3 2021 and those for Black people until Q1 2022 (1.3 percentage points against 1.1 percentage points). In Q2 2022, the recovery of the employment-to-population ratio slowed down or even receded marginally for all groups. In June 2022, the figure was still below pre-crisis levels for all three groups, standing at 58.6% for Black people, 59.9% for white people and 63.7% for Hispanic/Latino people.

Source: OECD Employment Outlook 2022, Chapter 1.

Labour market concentration, where few employers compete for workers, contributes to employer monopsony power. Monopsonistic employers can set wages unilaterally, leading to lower employment and wages. The largest cross-country analysis to date shows 16% of workers are employed in at least moderately concentrated labour markets. Reducing anticompetitive practices and expanding collective bargaining, among other policies, can curb monopsony power.

The United States’ business sector is slightly more concentrated than the OECD average. 17% of employees in the United States work in concentrated labour markets (in contrast to 16% across OECD countries).

Greater labour market concentration is linked to detrimental impacts on job quality. For example, recent literature estimating the impact of local labour market concentration on wages in the United States shows that doubling labour market concentration reduces wages by 1-5%. In addition, there is evidence from job postings data in the United States that employers require more skills from workers when labour markets become more concentrated.

To ameliorate the problem of growing labour market concentration, the US administration has undertaken bold actions in terms of antitrust enforcement. If consistently applied, these actions are likely to improve wages and working conditions in the long run.

Other policy options to counteract labour market concentration also warrant consideration. Of particular importance in the high-inflation context, policies to reduce the wage setting power of firms with dominant labour market positions could help to raise wages and reduce wage inequality. In addition, collective bargaining plays a key role in countervailing monopsony power. Additional legislation encouraging collective bargaining and enhancing its coverage could be considered to dampen the consequences of concentration. Finally, existing evidence from the United States suggests that making non-compete agreements (NCAs) less enforceable would unambiguously increase job mobility and raise wages.

Contact

Stefano SCARPETTA (✉ [email protected])

Anna MILANEZ (✉ [email protected])

Andrew GREEN (✉ [email protected])